| Latest | Greatest | Lobby | Journals | Search | Options | Help | Login |

|

|

|

This topic is archived. |

| Home » Discuss » Topic Forums » Economy |

|

| Robert Oak

|

Sat Mar-05-05 01:00 PM Original message |

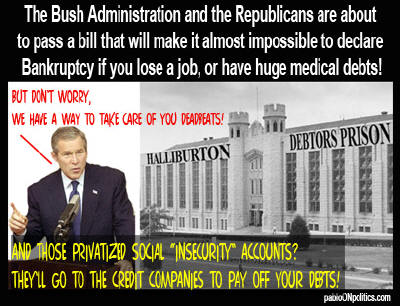

| Bankruptcy, outrage, congress allows 30% interest rate |

| Printer Friendly | Permalink | | Top |

| BlueEyedSon

|

Sat Mar-05-05 01:02 PM Response to Original message |

| 1. Pretty obvious who our legislators are working for these days..... |

| Printer Friendly | Permalink | | Top |

| n2mark

|

Sat Mar-05-05 01:04 PM Response to Original message |

| 2. Thanks pukes |

| Printer Friendly | Permalink | | Top |

| murray hill farm

|

Sat Mar-05-05 01:04 PM Response to Original message |

| 3. How does bankruptsy work? |

| Printer Friendly | Permalink | | Top |

| Vincardog

|

Sat Mar-05-05 01:15 PM Response to Reply #3 |

| 6. It depends on where you live and on which type of bankruptcy you file. |

| Printer Friendly | Permalink | | Top |

| murray hill farm

|

Sat Mar-05-05 01:38 PM Response to Reply #6 |

| 10. Thanks! |

| Printer Friendly | Permalink | | Top |

| happyslug

|

Sun Mar-06-05 02:29 AM Response to Reply #10 |

| 18. Chapter 11 is reserved for Corporations |

| Printer Friendly | Permalink | | Top |

| NMDemDist2

|

Sat Mar-05-05 01:15 PM Response to Reply #3 |

| 7. that's what it USED to mean |

| Printer Friendly | Permalink | | Top |

| Robert Oak

|

Sat Mar-05-05 01:35 PM Response to Reply #3 |

| 8. secured debt versus unsecured debt |

| Printer Friendly | Permalink | | Top |

| murray hill farm

|

Sat Mar-05-05 01:42 PM Response to Reply #8 |

| 14. Thank u so much... |

| Printer Friendly | Permalink | | Top |

| happyslug

|

Sun Mar-06-05 02:08 AM Response to Reply #3 |

| 17. Bankruptcy has existed since Queen Elizabeth Reign |

| Printer Friendly | Permalink | | Top |

| da_chimperor

|

Sat Mar-05-05 01:12 PM Response to Original message |

| 4. My my, what a fine job of looking out for their campaign donors |

| Printer Friendly | Permalink | | Top |

| HereSince1628

|

Sat Mar-05-05 01:14 PM Response to Original message |

| 5. My copy of the bible is pretty clear on condemning usury, suppose |

| Printer Friendly | Permalink | | Top |

| Robert Oak

|

Sat Mar-05-05 01:38 PM Response to Reply #5 |

| 11. freepers have grabbed a few issues and use them |

| Printer Friendly | Permalink | | Top |

| Name removed

|

Sat Mar-05-05 01:38 PM Response to Original message |

| 9. Deleted message |

| Robert Oak

|

Sat Mar-05-05 01:40 PM Response to Reply #9 |

| 13. that's different, try being a consultant |

| Printer Friendly | Permalink | | Top |

| HereSince1628

|

Sat Mar-05-05 01:46 PM Response to Reply #9 |

| 16. Yes, but that's a risk of offering credit |

| Printer Friendly | Permalink | | Top |

| lastknowngood

|

Sat Mar-05-05 01:38 PM Response to Original message |

| 12. Really there is no limit if they wish to charge you 500% that's fine |

| Printer Friendly | Permalink | | Top |

| Robert Oak

|

Sat Mar-05-05 01:45 PM Response to Reply #12 |

| 15. "credit score" |

| Printer Friendly | Permalink | | Top |

| nathansnewman

|

Sun Mar-06-05 10:50 AM Response to Original message |

| 19. Santorum's pro-Sweatshop Amendments |

| Printer Friendly | Permalink | | Top |

| Robert Oak

|

Sun Mar-06-05 11:45 AM Response to Reply #19 |

| 20. @^&($^ Thank you, this is important |

| Printer Friendly | Permalink | | Top |

| DU_ONE

|

Sun Mar-06-05 12:27 PM Response to Original message |

| 21. illegal to go broke |

| Printer Friendly | Permalink | | Top |

| DU

AdBot (1000+ posts) |

Tue Apr 30th 2024, 10:20 AM Response to Original message |

| Advertisements [?] |

| Top |

| Home » Discuss » Topic Forums » Economy |

|

Powered by DCForum+ Version 1.1 Copyright 1997-2002 DCScripts.com

Software has been extensively modified by the DU administrators

Important Notices: By participating on this discussion board, visitors agree to abide by the rules outlined on our Rules page. Messages posted on the Democratic Underground Discussion Forums are the opinions of the individuals who post them, and do not necessarily represent the opinions of Democratic Underground, LLC.

Home | Discussion Forums | Journals | Store | Donate

About DU | Contact Us | Privacy Policy

Got a message for Democratic Underground? Click here to send us a message.

© 2001 - 2011 Democratic Underground, LLC