| Latest | Greatest | Lobby | Journals | Search | Options | Help | Login |

|

|

|

This topic is archived. |

| Home » Discuss » Archives » General Discussion (1/22-2007 thru 12/14/2010) |

|

| HCE SuiGeneris

|

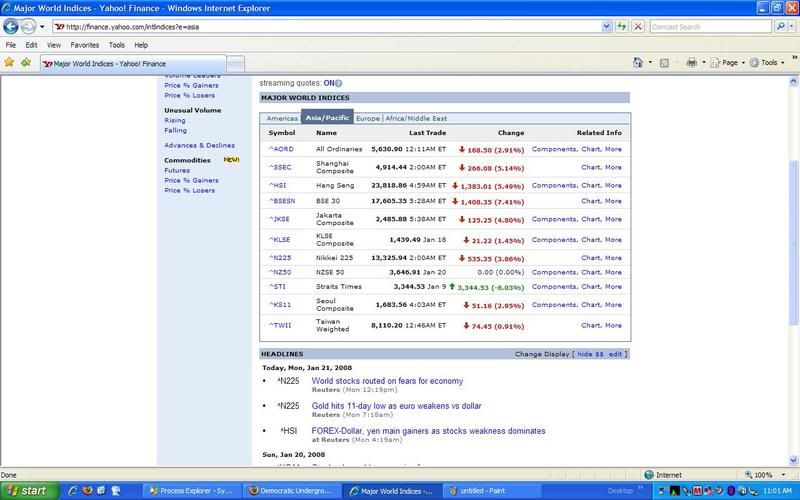

Mon Jan-21-08 01:08 PM Original message |

| Don't Look Too Closely... This Is Very Scary, Another Black Tuesday Looms |

| Printer Friendly | Permalink | | Top |

| tekisui

|

Mon Jan-21-08 01:09 PM Response to Original message |

| 1. It will not be pretty. |

| Printer Friendly | Permalink | | Top |

| HCE SuiGeneris

|

Mon Jan-21-08 01:12 PM Response to Reply #1 |

| 4. To take a screen shot |

| Printer Friendly | Permalink | | Top |

| tekisui

|

Mon Jan-21-08 01:17 PM Response to Reply #4 |

| 6. Thanks, I've wondered how to for awhile. |

| Printer Friendly | Permalink | | Top |

| Gman

|

Mon Jan-21-08 01:10 PM Response to Original message |

| 2. It won't be pretty in the morning |

| Printer Friendly | Permalink | | Top |

| HCE SuiGeneris

|

Mon Jan-21-08 01:13 PM Response to Reply #2 |

| 5. That news was what prompted this post. Yikes! |

| Printer Friendly | Permalink | | Top |

| lovuian

|

Mon Jan-21-08 01:11 PM Response to Original message |

| 3. Agree |

| Printer Friendly | Permalink | | Top |

| LulaMay

|

Mon Jan-21-08 01:18 PM Response to Original message |

| 7. Should I take my money out of CD's? |

| Printer Friendly | Permalink | | Top |

| ramapo

|

Mon Jan-21-08 01:23 PM Response to Reply #7 |

| 10. No |

| Printer Friendly | Permalink | | Top |

| melody

|

Mon Jan-21-08 01:27 PM Response to Reply #10 |

| 15. Terrific post -- agree completely n/t |

| Printer Friendly | Permalink | | Top |

| LulaMay

|

Mon Jan-21-08 01:34 PM Response to Reply #10 |

| 23. I have debt and savings.....how much debt should I pay down, how much should I save? |

| Printer Friendly | Permalink | | Top |

| spotbird

|

Mon Jan-21-08 01:59 PM Response to Reply #23 |

| 33. There is no safe investment that |

| Printer Friendly | Permalink | | Top |

| ramapo

|

Mon Jan-21-08 02:03 PM Response to Reply #23 |

| 34. I really can't answer that but.... |

| Printer Friendly | Permalink | | Top |

| SoCalDem

|

Mon Jan-21-08 05:02 PM Response to Reply #23 |

| 53. $10K in credit card debt? and $75K in CDs? |

| Printer Friendly | Permalink | | Top |

| dchill

|

Mon Jan-21-08 03:14 PM Response to Reply #10 |

| 47. "...save some money..." |

| Printer Friendly | Permalink | | Top |

| MattSh

|

Tue Jan-22-08 07:31 AM Response to Reply #10 |

| 59. Dollars can be a risk too. Just saying. |

| Printer Friendly | Permalink | | Top |

| Liberal In Texas

|

Tue Jan-22-08 08:08 AM Response to Reply #59 |

| 61. There is ONE bank in the US that sells CDs in foreign currency. |

| Printer Friendly | Permalink | | Top |

| HCE SuiGeneris

|

Mon Jan-21-08 01:24 PM Response to Reply #7 |

| 12. CD's are not affected by the stock market |

| Printer Friendly | Permalink | | Top |

| LulaMay

|

Mon Jan-21-08 01:30 PM Response to Reply #12 |

| 17. Thank you. I wondered if it was so bad there was any chance banks might fail. |

| Printer Friendly | Permalink | | Top |

| HCE SuiGeneris

|

Mon Jan-21-08 01:36 PM Response to Reply #17 |

| 24. The other post to your question from ramapo (above) |

| Printer Friendly | Permalink | | Top |

| nashville_brook

|

Mon Jan-21-08 01:34 PM Response to Reply #12 |

| 22. as "cheap money" disappears, shouldn't CD interest rates increase? |

| Printer Friendly | Permalink | | Top |

| HCE SuiGeneris

|

Mon Jan-21-08 01:41 PM Response to Reply #22 |

| 27. Some info |

| Printer Friendly | Permalink | | Top |

| nashville_brook

|

Mon Jan-21-08 01:52 PM Response to Reply #27 |

| 30. yeah -- i know you get better rates for a longer commitment -- but, i'm talking about the effect of |

| Printer Friendly | Permalink | | Top |

| HCE SuiGeneris

|

Mon Jan-21-08 02:03 PM Response to Reply #30 |

| 35. Double digit CD rates will probably not be seen again (IMHO) |

| Printer Friendly | Permalink | | Top |

| FarCenter

|

Mon Jan-21-08 02:53 PM Response to Reply #35 |

| 43. It depends on the rate of inflation |

| Printer Friendly | Permalink | | Top |

| tnlurker

|

Mon Jan-21-08 01:21 PM Response to Original message |

| 8. I moved all of my 401K money last week |

| Printer Friendly | Permalink | | Top |

| Tiberius

|

Mon Jan-21-08 01:39 PM Response to Reply #8 |

| 25. I did the same |

| Printer Friendly | Permalink | | Top |

| kamtsa

|

Mon Jan-21-08 02:22 PM Response to Reply #8 |

| 36. If you are a long time investor, read this ... |

| Printer Friendly | Permalink | | Top |

| tnlurker

|

Mon Jan-21-08 02:28 PM Response to Reply #36 |

| 37. Thanks |

| Printer Friendly | Permalink | | Top |

| olddad56

|

Mon Jan-21-08 02:41 PM Response to Reply #36 |

| 40. I put my 401K in cahs 3 months ago ... |

| Printer Friendly | Permalink | | Top |

| kamtsa

|

Mon Jan-21-08 03:17 PM Response to Reply #36 |

| 49. Three more points ... |

| Printer Friendly | Permalink | | Top |

| eridani

|

Tue Jan-22-08 08:14 AM Original message |

| Fine for long-termers |

| Printer Friendly | Permalink | | Top |

| eridani

|

Tue Jan-22-08 08:14 AM Response to Reply #36 |

| 62. Fine for long-termers |

| Printer Friendly | Permalink | | Top |

| olddad56

|

Mon Jan-21-08 02:35 PM Response to Reply #8 |

| 39. I don't think that bond funds will do well either. Even cash will lose out to inflation. |

| Printer Friendly | Permalink | | Top |

| papau

|

Mon Jan-21-08 01:21 PM Response to Original message |

| 9. India down 7% overnight is scary |

| Printer Friendly | Permalink | | Top |

| fasttense

|

Mon Jan-21-08 01:24 PM Response to Original message |

| 11. Welcome to the "free market's" great economy. |

| Printer Friendly | Permalink | | Top |

| high density

|

Mon Jan-21-08 01:25 PM Response to Original message |

| 13. That's good, I've got some money I want to dump in. NM |

| Printer Friendly | Permalink | | Top |

| joeglow3

|

Mon Jan-21-08 01:30 PM Response to Reply #13 |

| 18. Amen. Clearance sale. Everything must go. nt |

| Printer Friendly | Permalink | | Top |

| inanna

|

Mon Jan-21-08 01:25 PM Response to Original message |

| 14. Recommended. |

| Printer Friendly | Permalink | | Top |

| bdamomma

|

Mon Jan-21-08 01:27 PM Response to Original message |

| 16. not good at all, almost makes a person think this is what |

| Printer Friendly | Permalink | | Top |

| Pathwalker

|

Mon Jan-21-08 01:32 PM Response to Reply #16 |

| 21. They have repeatedly admitted this is the plan, so NO |

| Printer Friendly | Permalink | | Top |

| HCE SuiGeneris

|

Mon Jan-21-08 01:45 PM Response to Reply #16 |

| 28. Those with the fattest purses and "right" connections |

| Printer Friendly | Permalink | | Top |

| tbyg52

|

Mon Jan-21-08 05:12 PM Response to Reply #28 |

| 54. Tell me |

| Printer Friendly | Permalink | | Top |

| bighughdiehl

|

Mon Jan-21-08 01:31 PM Response to Original message |

| 19. Eh.... |

| Printer Friendly | Permalink | | Top |

| Miss Chybil

|

Mon Jan-21-08 01:31 PM Response to Original message |

| 20. Looks like a good time to buy. nt |

| Printer Friendly | Permalink | | Top |

| the other one

|

Mon Jan-21-08 01:39 PM Response to Reply #20 |

| 26. HAHAHAHAHAHAHAHAHA!!! |

| Printer Friendly | Permalink | | Top |

| high density

|

Mon Jan-21-08 01:49 PM Response to Reply #26 |

| 29. You're Hilarious |

| Printer Friendly | Permalink | | Top |

| safeinOhio

|

Mon Jan-21-08 01:56 PM Response to Reply #29 |

| 32. Gold down to 864 |

| Printer Friendly | Permalink | | Top |

| harun

|

Mon Jan-21-08 01:56 PM Response to Reply #20 |

| 31. A contrarian thinker, just like me (n/t) |

| Printer Friendly | Permalink | | Top |

| Eurobabe

|

Mon Jan-21-08 02:31 PM Response to Original message |

| 38. Great balls of FIRE, the DAX had it's biggest point drop EVA |

| Printer Friendly | Permalink | | Top |

| olddad56

|

Mon Jan-21-08 02:45 PM Response to Original message |

| 41. It will be interesting to see what the Federal Reserve bank does to make it worse. |

| Printer Friendly | Permalink | | Top |

| fshrink

|

Mon Jan-21-08 02:48 PM Response to Original message |

| 42. It's quite simple really: |

| Printer Friendly | Permalink | | Top |

| Hulk

|

Mon Jan-21-08 03:01 PM Response to Original message |

| 44. Doesn't look so bad at the moment, down 59 points, but..... |

| Printer Friendly | Permalink | | Top |

| GOPNotForMe

|

Mon Jan-21-08 03:16 PM Response to Reply #44 |

| 48. That 59-point drop was Friday. U.S. market's closed today. nt |

| Printer Friendly | Permalink | | Top |

| sarcasmo

|

Mon Jan-21-08 03:02 PM Response to Original message |

| 45. I was going to post this too, Thanks for doing it Kick and Nom |

| Printer Friendly | Permalink | | Top |

| smoogatz

|

Mon Jan-21-08 03:11 PM Response to Original message |

| 46. Gas, guns and water. |

| Printer Friendly | Permalink | | Top |

| dchill

|

Mon Jan-21-08 03:19 PM Response to Original message |

| 50. Moved? I guess this isn't news. |

| Printer Friendly | Permalink | | Top |

| benld74

|

Mon Jan-21-08 03:37 PM Response to Original message |

| 51. TIIIIIMMBBEERRRRRRRRRRRR! |

| Printer Friendly | Permalink | | Top |

| sarcasmo

|

Mon Jan-21-08 04:58 PM Response to Original message |

| 52. This needs a KICK. |

| Printer Friendly | Permalink | | Top |

| Tierra_y_Libertad

|

Mon Jan-21-08 05:16 PM Response to Original message |

| 55. Do not stand under tall buildings with windows. Stockbrokers can be heavy when falling. |

| Printer Friendly | Permalink | | Top |

| and-justice-for-all

|

Mon Jan-21-08 08:31 PM Response to Original message |

| 56. Will Roth and IRAs be affected? |

| Printer Friendly | Permalink | | Top |

| file83

|

Tue Jan-22-08 12:53 AM Response to Reply #56 |

| 57. Yup. |

| Printer Friendly | Permalink | | Top |

| Narkos

|

Tue Jan-22-08 01:10 AM Response to Original message |

| 58. Ahhhh, this reeeeeaaallllllly sucks |

| Printer Friendly | Permalink | | Top |

| Perry Logan

|

Tue Jan-22-08 07:35 AM Response to Original message |

| 60. Got my fingers crossed here. |

| Printer Friendly | Permalink | | Top |

| DU

AdBot (1000+ posts) |

Sat May 04th 2024, 08:11 AM Response to Original message |

| Advertisements [?] |

| Top |

| Home » Discuss » Archives » General Discussion (1/22-2007 thru 12/14/2010) |

|

Powered by DCForum+ Version 1.1 Copyright 1997-2002 DCScripts.com

Software has been extensively modified by the DU administrators

Important Notices: By participating on this discussion board, visitors agree to abide by the rules outlined on our Rules page. Messages posted on the Democratic Underground Discussion Forums are the opinions of the individuals who post them, and do not necessarily represent the opinions of Democratic Underground, LLC.

Home | Discussion Forums | Journals | Store | Donate

About DU | Contact Us | Privacy Policy

Got a message for Democratic Underground? Click here to send us a message.

© 2001 - 2011 Democratic Underground, LLC